- Day 1 – What’s Travel Hacking all about?

- Day 2 – Getting Organized

- Day 3 – Types of Miles and Points

- Day 4 – Credit Card Strategy

- Day 5 – Southwest Companion Pass

- Day 6 – Business Credit Cards

- Day 7 – Hotel Free Night Sign-Up Bonuses & Annual Certificates

Some of the offers mentioned below (including the Chase Hyatt Visa example below) may be expired or not available.

I made a mistake when I first got into this hobby. I had applied for a certain credit card and met a $5000 spending requirement but the bonus points didn’t post to my account. Confused, I called up and was told that I wasn’t eligible for the sign-up bonus because I had received the sign up bonus for the same card 18 months prior.

I had forgotten all about this and hadn’t kept track of the credit cards I was getting and bonuses I received. After this mishap, I began tracking every single credit card on a spreadsheet and taking screenshots of every credit card application.

In this lesson, I’ll show you a few techniques that I use when applying for a new credit card and keeping track of the card details.

Applying

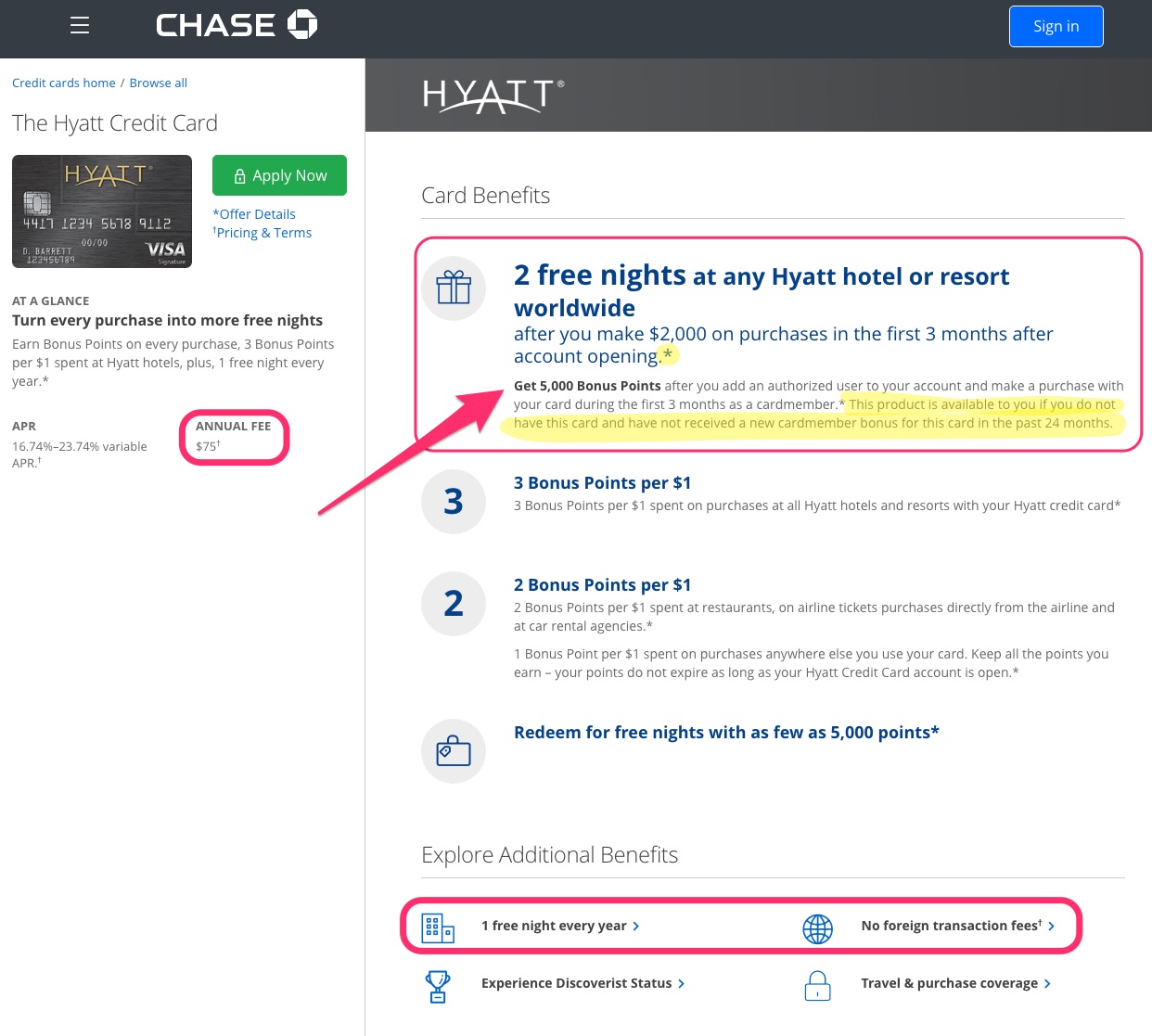

Let’s go back our example in the previous lesson – the Chase Hyatt Visa. Here is the information page at the Chase website. There are few items to take note of:

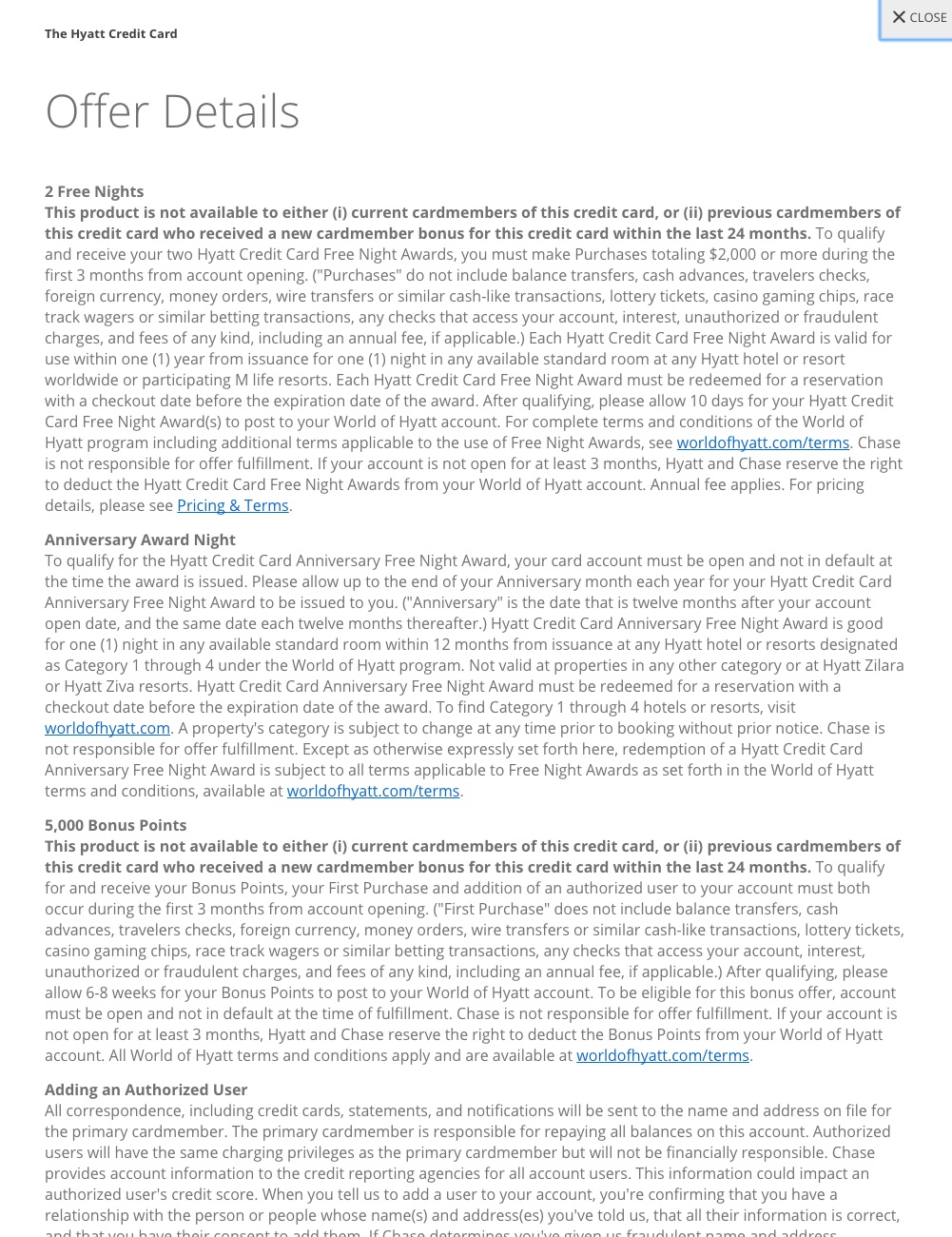

- Sign-up Bonus – 2 free nights at ANY Hyatt hotel worldwide after making $2000 in purchases in the first 3 months. Notice the highlighted ‘*’ section – you won’t receive the sign-up bonus if you have or had this card and received the bonus in the past 24 months.

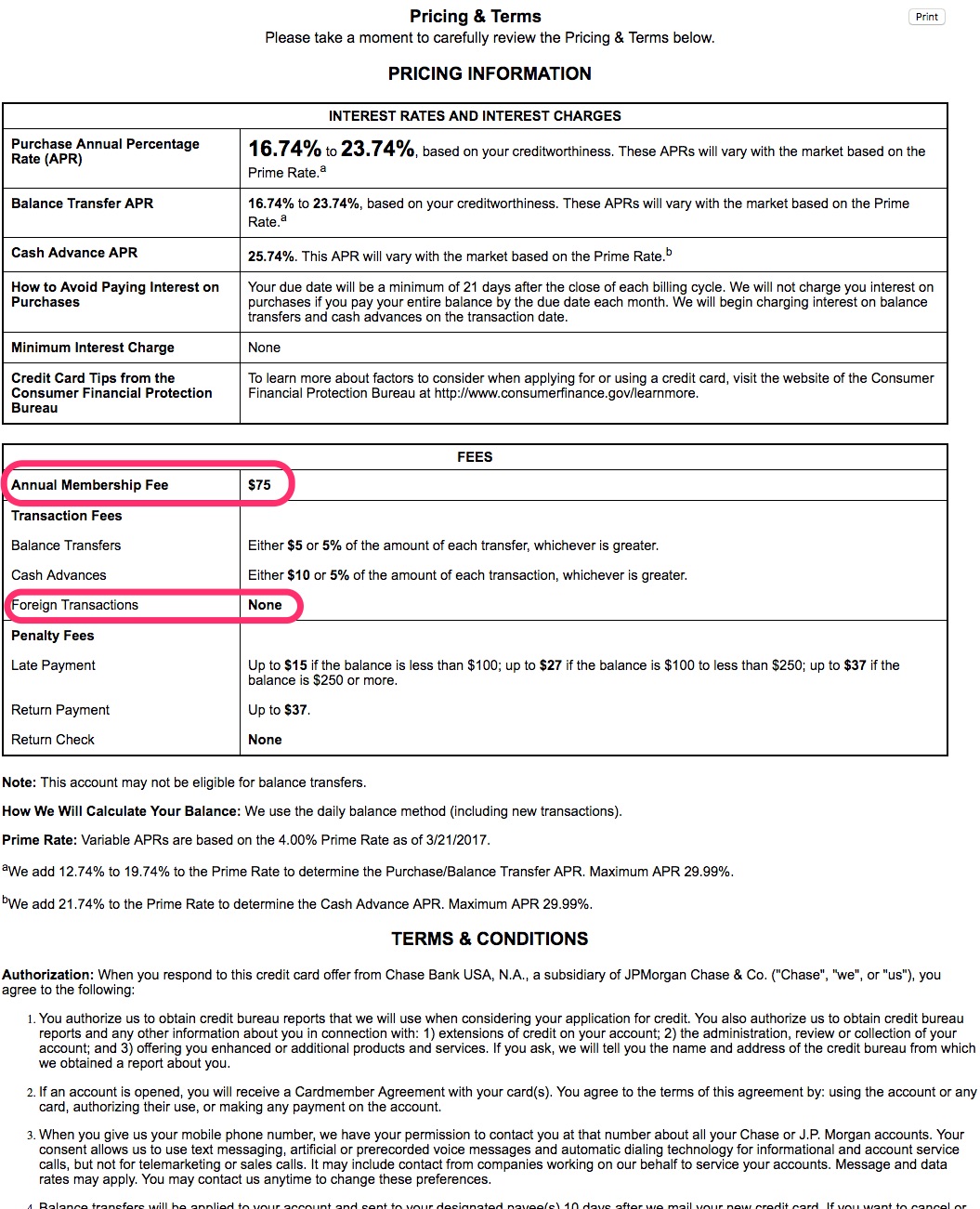

- Annual Fee – $75. Some credit cards will waive the annual fee the first year. This particular one does NOT so you will be charged the $75 annual fee in your first billing cycle.

- Authorized User Bonus – this credit card is also giving you 5000 bonus points after you add an authorized user to your account and they make a purchase during the first 3 months. This is an extra easy 5000 points – simply during the application process add your spouse, child, friend, etc as an authorized user. You will then receive two cards in the mail instead of one. You don’t even have to give them the credit card, just make a single purchase (a coffee, an itunes app, etc) with that second card and put it in your credit card holder case.

- Bonus Point Categories – typically credit cards offer additional points in certain categories. In the example above you will earn 3 points per $1 spend at all Hyatt hotels and 2 points per $1 spent at restaurants, airline tickets and car rental agencies.

- Cardmember Anniversary Bonus – some credit cards offer you a bonus each year you stay a member and pay the annual fee. Chase Hyatt provides a free night at a category 1-4 hotel each year. Another example would be the Chase Southwest card providing you will 6000 Southwest points each year.

- Foreign Transaction Fee – if you do International traveling, this is a nice benefit to have no foreign transaction fees. ALWAYS pay in the local currency and Visa/Mastercard will convert it to USD with no additional fees and give you a great conversion rate.

- APR – I never look at this because I never pay interest. Make sure you always pay your full credit card bill each month so you don’t incur interest charges. All of these bonus will be for not if you are paying 16%-24% interest payments.

I always take a screenshot of the offer details before I start the application process just in case a sign-up bonus doesn’t post for some reason so I have proof of what I applied for. Luckily I’ve never had a problem with a sign-up bonus not posting, other than the mistake I made that I shared at the beginning of this lesson.

If you forgot to take a screenshot of the offer or wanted to confirm your sign-up offer, there are a few things you can do:

- When you call to activate your card, although most activation lines are automated, you can transfer to a live agent who can look up what your sign-up offer was.

- You can chat from within your credit card account. A lot of the major credit card companies have an online chat function after you login to your account. Simply chat with the agent saying you recall there was a new cardmember bonus when you applied but can’t remember the details. They will quickly pull up your offer details for you. This saves your from making a call, navigating an automated phone system, and waiting for a live agent.

- You can also send a secure message from within your credit card account. Simply send a message saying you recall there was a new cardmember bonus when you applied but can’t remember the details. I’ve always received a prompt response that outlined the offer details I prefer this method best as I now have written proof of the offer details.

The Fine Print

Did you notice the ‘Offer Details’ and ‘Pricing & Terms’ links under the ‘Apply Now’ button? If you looking for some light reading before bed, this is for you 😉 Some people are adamant about ready every single line of the fine print. I read through a few of these when I first started out but quickly got bored of them. I think the main application page does a decent job of showing you the important this.

A lot of beginner’s questions can be answered if the fine print. Let’s see if you can answer these:

- Does the $75 annual fee that is charged during the first month count towards the $2000 in 3 month spending requirement?

- It’s been exactly one year since my account was opened, but I didn’t get my free night certificate?

- I got my two free night awards but the 5000 bonus points didn’t post to my account even though I added an authorized user and a purchase was made with the authorized user’s card.

Answers

- Does the $75 annual fee that is charged during the first month count towards the $2000 in 3 month spending requirement? No, the annual fee does NOT count towards the $2000 in purchases. Neither does balance transfers or cash advances.

- It’s been exactly one year since my account was opened, but I didn’t get my free night certificate? Please allow up to the end of your Anniversary month each year for the free night award to be issued to you.

- I got my two free night awards but the 5000 bonus points didn’t post to my account even though I added an authorized user and a purchase was made with the authorized user’s card. Please allow 6-8 weeks for your bonus points to post to your World of Hyatt account after qualifying.

Hotel/Airline Loyalty Account #

A common problem with beginners when applying for new hotel and airline credit cards is they forget to fill in their frequent flier number or hotel loyalty membership number on the credit card application.

If you already have a World of Hyatt account number, be sure to fill it in on the Chase Hyatt credit card application. If you don’t you will be assigned a new World of Hyatt account number and end up with two loyalty accounts at Hyatt. It’s an extra step and sometimes a pain to get two accounts combined.

Time Requirement

Just about all of the sign-up bonuses have a time requirement in addition to the spending requirement – i.e. $5000 in 3 months. But how exactly is the 3 month period calculated? Is it 3 months from

- the day I applied for the card?

- the day I am approved for the card?

- the day I receive the card in the mail?

- the day I activate the new credit card?

- the day of my first statement closing date?

- the day my annual fee posts to my account?

Typically the time period starts from the day you are approved for the card. You may know this if you are immediately approved during online application process.

If not automatically approved, you will usually get a message saying ‘thank you for your application, we need to review your application further and will provide a response by mail within 7-10 days’. And your new card arrives in the mail a week later. So your approval date is sometime in between the day you applied for the card and day you receive it in the mail.

You can always call up and ask or send a secure message to find out the exact date you need to meet the spending requirement. To keep things simple, I just use the earliest possible date (the day I apply for a card) as the start of the time period.

I also like to complete my spending requirements as quick as possible and not wait until the very end. I’ve heard of stories of people thinking they met the spending requirement on the very last day only to find out that sometimes charges take a couple days to actually post to your account and they missed out on the bonus – DON’T BE THAT PERSON!

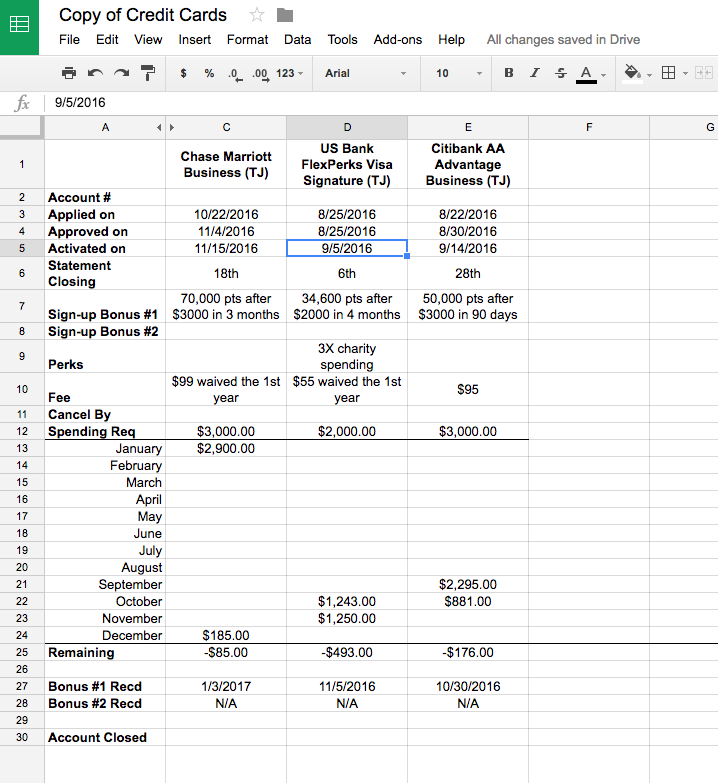

Keeping Track

So how do you keep track of all of these dates, spending requirements, etc?

I created a simple Google Documents spreadsheet – which lists what the card is, when I applied, when I was approved, activated the card, what the sign up bonus is, how much I need to spend to get the signup bonus, etc.

Click here to download a copy of my spreadsheet.

Here’s an example of what I use:

- Row 1 – the bank and credit card type. I used to put my name or my wife’s name in ( )s but the list of credit cards quickly got too long so I separated her cards on one tab and mine on another tab in the spreadsheet

- Row 2 – last 4 digits of the credit card

- Row 3 – date I applied for the card

- Row 4 – date I was approved for (if I know)

- Row 5 – date I activated the credit card

- Row 6 – which day of month the statement closes on

- Row 7 – what the main sign-up bonus is

- Row 8 – if there is a secondary sign-up bonus (like the 5000 points for adding an authorized user in the above Chase Hyatt example)

- Row 9 – any special perks of the card (bonus points for certain categories, free checked bag on an airline, free hotel status, etc)

- Row 10 – the annual fee and if it is waived the first year

- Row 11 – cancel by date, typically one year from application date. This is not as important since almost every credit card issuer has a grace period where they will refund the annual fee that posts to your account if you cancel within 30 days of the annual fee posting to your account.

- Row 12 – what the spending requirement is

- Rows 13-24 – how much spending I put on the card during each month’s statement closing

- Row 25 – automatically will subtract the total of rows 13-24 from row 12 so you know how much spending you still need to put on a card to earn the sign-up bonus. when it’s negative, you’ve met the requirement

- Row 27 & 28 – the date the sign-up bonus is received. Remember in the Chase Hyatt example above you are not eligible for a bonus if you received it within the past 24 months.

- Row 30 – the date I closed the account or I will simple write ‘USING’ in this box if it is a card a keep every year.

YOUR Beginner’s Strategy

My recommendation for beginners is to keep it simple when starting out. Plan to apply for just a single credit card to start with. Or if you have a spouse/partner, you can enter ‘two-player mode’ and have them also apply for a single credit card in their own name.

If you are in two-player mode, only apply for if you are comfortable meeting the minimum spending requirements on both cards in order to receive the sign-up bonus.

After getting approved, you will put ALL of your spending, no matter how small, on this card for the next few months until you hit the sign-up bonus spending requirement. Typically the requirements for sign-up bonuses are to complete a certain amount of spending ($2000, $3000, etc) in a certain time frame (usually 3 months). Your plan is to then apply for another credit card every 3 months for a total of 4 cards per year (or 8 total cards if you are in two-player mode).

Check Your Current Status

Before you apply for any cards, it’s a good practice to check your current credit card status. I recommend using Experian’s free account to verify how many credit cards you may already have or unknowingly opened in the past. Remember that 30% discount the cashier might have sold you on at a clothing store for opening a credit card?

Here is a step by step guide to how to check to see how many credit cards you have opened along with the date it was opened. If you are absolutely positive you haven’t opened any new credit cards in the past two years you can skip this step.

There are a couple of questions you have to ask yourself before picking your first card to apply for.

Business?

First – Can you apply for business credit cards?

Remember from the business cards lesson – you might already have a business and not know it. I highly recommend a ‘side hustle’ business so you can earn lots more miles and points with business credit cards.

If you answered no, move down to the ‘Personal Cards’ section below.

Next – Do you want to earn the Southwest Companion Pass? Do you live near an airport with lots of Southwest non stop flights? And do you have a companion you would like to travel with you for FREE?

If you answered no, move down to the ‘Have a Business’ section below.

If the answer to both of these questions is YES and it’s early in the year, I recommend applying for the Southwest Premier Business card first followed by one of the three Southwest Personal cards (Priority, Premier, or Plus). Obtaining and meeting the sign-up bonus requirements for both of these cards will likely get you the 110,000 miles required (or get your really close) for the Southwest Companion Pass.

If it’s late in the year (July-December), I would recommend waiting on both of these cards until January of the following year so you can maximize it’s value. Remember the companion pass is good for the rest of the year that you obtain the 110,000 miles as well as the entire following year. The earlier in the year you get it, the longer you can take advantage of it.

Just make sure you don’t go above 5/24 (opened 5 new credit cards within 24 months) or you won’t be able to get the Chase Southwest cards.

Apply for Chase Southwest Credit Cards:

- Southwest Rapid Rewards Premier Business ($99) and ONE OF THE FOLLOWING:

- Southwest Rapid Rewards Priority ($149)

- Southwest Rapid Rewards Plus ($69)

- Southwest Rapid Rewards Premier ($99)

Have a Business?

If you are not really interested in the Southwest Companion Pass but have a business. Your first card should be a Chase Business card. If you don’t have a business, move down to the ‘Personal Cards’ section below.

Since Chase implemented their 5/24 rule, you will want to apply for business cards that do not show up on your personal credit report first so they are NOT counted by Chase.

Remember only Barclay, Capital One, and Discover report business card to your personal credit report so DO NOT apply for any of those. All other issuers are fair game (American Express, Chase, Citi, Bank of America, etc)

Chase currently has six different business credit cards – three earn Chase’s flexible currency Ultimate Rewards and the other three are co-branded cards (United, Marriott, & Southwest).

When my status fell below 5/24, I applied for the Ink Business Preferred which offered 80,000 Chase Ultimate Reward Points as the sign up bonus.

Then two months later, I was instantly approved for the Ink Business Unlimited which had a 50,000 Chase Ultimate Reward Points sign up bonus to go along with 1.5% points on all purchases. These 50,000 Ultimate Reward Points can be transferred to United.

My next Chase Business card with probably be the United Explorer card since it is offering a 75,000 United miles sign up bonus.

In case the offer decreases by the time I apply, I might end up applying for the third Chase Ultimate Rewards card – the Ink Business Cash which offers 50,000 points to go along with 5% points in rotating quarterly categories.

Apply for Chase Business Credit Cards:

- Ink Business Preferred

- Ink Business Unlimited

- Ink Business Cash

- United Explorer Business

- Southwest Rapid Rewards Premier Business

- Marriott Bonvoy Premier Plus Business

Word of Caution – if you are meeting the sign up bonuses quickly and applying for cards quicker than every three months, I would sprinkle in other business credit cards between the Chase applications. I personally have three Chase Business credit cards. I’ll try for my fourth soon but that may be pushing my luck with Chase.

Next, continue to work through all business credits that don’t report to your personal credit report. Remember American Express allows only one bonus per lifetime per each card.

Other banks also have rules that restrict how often you can get a sign-up bonus so make sure these bonus cards are the highest (or near the highest) ever offered. Doctor of Credit periodically updates this spreadsheet that lists the highest offers ever on credit cards so you can compare the current offer to.

Personal Cards

If you don’t have a business (and don’t want to open one), your application strategy will revolve around personal credit cards. And due to the banks rules, you will definitely want to apply for Chase credit cards first since Chase implemented the 5/24 rule (Chase won’t approve you for their credit cards if you have opened five or more credit cards in the past 24 months so check your status at Experian).

Depending if you tried to obtain the Southwest Companion Pass in step 1, your 5/24 status should be 0/24 or 1/24 (one Chase personal Southwest credit card). This means you can get four or five more Chase personal credit cards before they will not approve you for any more.

Chase offers a BOATLOAD of personal credit cards. Since you are only going to be able to get five, you want to make sure you get the best. I recommend the Chase cards that offer flexible Ultimate Rewards so you can transfer them to airline and hotel partners. I recommend starting with one of Sapphire cards (remember Chase limits to only one at a time).

First – Chase Sapphire Cards

The Chase Sapphire Preferred and Chase Sapphire Reserve both typically offer a 50,000 Ultimate Reward sign up bonus (the Reserve card actually offered 100,000 sign up bonus when it first launched but I doubt it will ever be offered again).

The Reserve has a big $450 annual fee, but don’t be scared by it. It also comes with a $300 annual travel credit ($300 is automatically credited to your account when you make travel purchases) which really knocks the annual fee down to $150 per year. The Reserve also gives you 3X points on travel and dining purchases. Finally if you don’t transfer your Ultimate rewards to travel partners and instead use them at the Chase travel portal they are worth 50% more – meaning the 50,000 point sign up bonus is worth $750 at the Chase travel portal.

The Reserve also pays your $100 fee for Global Entry or TSA Precheck so you can use the short security line at airports. It also comes with airport lounge access through Priority Pass.

The Preferred has a much smaller annual fee at only $95 but there is NO travel credit like the reserve. You also earn only 2X points on travel and dining instead of 3X. And if you use your points at the Chase travel portal, they are worth 25% more – so the 50,000 point sign up bonus is worth $625 in travel.

It’s up to you to decide if the Reserve extra perks are worth the higher annual fee. I personally prefer the Reserve card.

Apply for Chase Sapphire Credit Cards:

Second, Third, (& Fourth) – Chase Co-Branded Cards

The next few personal Chase co-branded (hotel, airlines, Amazon, Disney, etc) credit cards that you get are really up to you and your personal preference. Some are better than others, some I would avoid at all cost. Let’s dig into the Co-Branded card types.

Hotel Cards

Looking the current sign up bonuses for each card, you might be thinking IHG is the best (at 80,000 point) and Hyatt is the worst (only 50,000 points) but you would be wrong. All points are not created equal and have different values.

Hyatt’s highest category hotel is a category 7 and costs 30,000 points per night. While IHG’s top category hotel costs 70,000 points. And Marriott’s highest category on peak hotel will cost a whopping 100,000 points in 2019.

Personally my first choice of all of the co-branded cards would be the World of Hyatt card. As you saw in the hotel free night sign up bonus and annual certificates lesson, you can score some really amazing Hyatt redemptions to go along with the free award night each year.

My second choice would be for the IHG Rewards Club Premier, I just don’t love Marriott as much as Hyatt or IHG.

One thing to remember is that Chase Ultimate Reward points (from the Sapphire cards) all transfer to Hyatt, Marriott, & IHG.

Apply for Chase Hotel Credit Cards:

Airline Cards

While there will be a bunch (10+) of different airline credit cards on Chase’s site, there are really only three airline frequent flier programs – Southwest Rapid Rewards miles, United miles, and Avios (British Airways, Aer Lingus, & Iberia). Just like the hotel cards, Chase Ultimate Reward points (from the Sapphire cards) all transfer to Southwest, United, & Avios.

Avios – all three frequent flier programs (British Airways, Aer Lingus, & Iberia) all use Avios as their points for their frequent flier programs. This makes is possible to transfer Avios between all three airline partners. You can use Avios to book flights on American Airlines.

The choice of which card to get will come down to personal preference – some people love Southwest while others hate it. Some people live near a United hub (Newark, San Francisco, Houston, Dulles, etc) and may fly United often.

Southwest Cards

Of the three Southwest credit cards, I would recommend the highest annual fee one – Rapid Rewards Priority. Even with a $149 annual fee, the ongoing perks that come with it are worth more than $149. Let’s take a look:

First it gives you a $75 Southwest annual travel credit.

It also gives you 7500 points each year on your cardmember anniversary. Southwest points are generally worth 1.6 cents each so 7500 points is worth $120.

Finally it also gives you four upgraded boarding positions each year. These are actually better than purchasing early bird since you will get boarding position A1-A15 when you purchase this at the check-in counter or ticket counter. While early bird is usually $15-$25, upgraded boardings cost $30-$50. For simplicity, let’s just say these are worth $15 (like the cheapest early bird).

$75 (travel credit) + $120 (7500 miles) + $60 (upgraded boarding) = $255 value vs $149 annual fee.

Apply for Chase Southwest Credit Cards:

- Chase Southwest Rapid Rewards Priority

- Chase Southwest Rapid Rewards Plus

- Chase Southwest Rapid Rewards Premier

United Cards

Of the three United credit cards, I would recommend either the United Explorer card ($95 annual fee) or if you are a die-hard United fan the United MileagePlus Club card ($450 annual fee).

The only reason to splurge on the United MileagePlus Club card is if you don’t have United elite status that already gets you into United Clubs since this card includes a $550 membership to United Clubs. It also gives you and your companion a second checked bag free (Explorer card only gives you one checked bag free).

I would stay away from the no annual fee United TravelBank card since it only earns 2% back with travel on United. You should already have a Sapphire card that earns 2X or 3X on ALL travel not just on United.

Personally I would apply for the standard United Explorer card – I rarely travel with more than one checked bag and use Priority Pass lounges (with Sapphire Reserve).

Apply for Chase United Credit Cards:

- Chase United Mileage Plus Club

- Chase United Explorer

- Chase United TravelBank

Avios Cards

At first glance, these cards seem to offer the highest sign up bonus – usually 100,000 miles. But after digging into the details there is a very large spending requirement to get those 100,000 miles.

In the offers above, you need to spend a whopping $20,000 to earn the full 100,000 miles. They do give you a full year to meet that requirement.

Getting this card may make sense if you fly out of an American Airlines city since Avios can be used to book American Airline flights. Also since all of the points transfer between all three programs it really doesn’t matter which you apply for – although British Airways website is the easiest to use of the three to make online award bookings.

Apply for Chase Avios Credit Cards:

- Chase British Airways Visa

- Chase Aer Lingus Visa

- Chase Iberia Visa

Other Chase Co-Branded Cards

I would NOT recommend applying for any of Chase’s other co-branded credit cards. You might be tempted when you see Starbucks or Disney thinking you go there a lot, but when you dig into the details, these are not very good credit cards.

A $50 statement credit or a few free drinks at Starbucks? You can do a lot better than that.

Apply for Other Chase Credit Cards:

- Don’t do it!

- Don’t do it!

- Don’t do it!

So how many co-branded Chase credit cards will you apply for? I would personally apply for at least two but no more than four of them. My top four are:

- Chase World of Hyatt

- Southwest Rapid Rewards Priority

- Chase United Explorer

- Chase IHG Rewards Club Premier

Fourth (& Fifth?) – Chase Freedom Cards

The next personal Chase credit card I would recommend applying for is one of the Freedom cards.

Cash Back or Ultimate Rewards?

After looking at the current offer, you might be thinking I thought he recommended Ultimate Reward but these cards offer cash back. That is true, but both of these cards actually earns Ultimate Reward points. If you don’t have one of Chase’s Sapphire cards, you would only be able to redeem the Freedom UltimateRewards for cash back.

For example, the $200 cash bonus listed above for the Chase Freedom Unlimited card is actually 20,000 Ultimate Reward points. You can transfer the 20,000 points to your Sapphire Reserve or Preferred card. Once with a Sapphire card, you could then transfer them to airline or hotel partners or use at the Chase travel portal for $300 in travel if you have the Reserve card (or $250 with the Preferred).

Which Freedom?

Back to the Freedom cards, the sign up bonus (typically 15,000 or 20,000 points) will be lower than the Sapphire cards since these are NO annual fee cards.

You will next want to decide on either the original Freedom card or the Freedom Unlimited card. The difference is the Freedom card earns 5% points on rotating quarterly categories (up to $1500 per quarter) and 1% on all other purchases while the Freedom Unlimited earns a flat 1.5% on ALL purchases.

I personally prefer the higher 5% rotating categories with the Freedom. It’s a little more work but gives you much better returns. Even though I may not typically spend $1500 per quarter in certain categories, I like to maximize it anyway – here’s how:

Amazon is almost always one of the rotating categories each year. While I usually don’t spend $1500 at Amazon in a 3 month period, I’ll buy an Amazon gift card to get to the $1500 threshold so I earn 7500 Chase Ultimate Reward points ($1500 x 5X points = 7500 Chase Ultimate Rewards) in the quarter. I’ll then just load the gift card to my account and use it during the rest of the year.

Now if you don’t want to remember which categories are in which quarter, you might be better with the Freedom Unlimited with its 1.5% points on ALL purchases the whole year.

I should mention that you can also downgrade either the Sapphire Reserve or Sapphire Preferred to one of the Freedom cards if you want to. But remember you have to have at least one premium card if you want to be able to transfer the points to travel partners. If you downgrade to a Freedom card you also will NOT get the 15,000 or 20,000 point sign up bonus.

Apply for Chase Freedom Credit Cards:

Two-Player Mode

I know there are a lot of choices, but don’t forget if you are in two-player mode (applying for cards with a spouse/partner) you can split up card choices. Maybe you get the Sapphire Reserve and your spouse gets the Sapphire Preferred. You get the original Freedom card, and they get the Freedom Unlimited card.

You get the United Explorer card and your spouse gets the Southwest Rapid Rewards Priority card. Most likely you will be traveling together anyway, so there is no need for both of you to get the United Explorer card since it allows your companion to also get a free checked bag too.

5 Chase Cards, Now What?

After your fifth Chase credit card, you will now be over their dreaded 5/24 rule and no longer be able to be approved for any more Chase cards. This should have taken you anywhere from 9 to 18 months to get to. Now it’s time to move on to other banks – and there are a BUNCH more.

Go back to the credit card rules lesson to refresh your memory. Here are the basics:

- Flexible currencies other than Chase Ultimate Rewards should be at the top of your list (American Express Membership Rewards, Citi Thank You Points, Capital One Miles).

- American Express cards are generally pretty easy to get approved for but make sure you apply for them when they have historically high welcome bonus offers since you can generally only obtain one American Express welcome bonus once per LIFETIME. (Doctor of Credit periodically updates this spreadsheet that lists the highest offers ever on credit cards so you can compare the current offer to.)

- Citibank has implemented restrictions on their best credit cards – you can only earn the sign-up bonus if you haven’t opened or closed that specific credit card family type in the past 24 months.

- Bank of America has the 2/3/4 rule. They will only approve you at most 2 cards per rolling 2 months, 3 cards per rolling 12 months, and 4 cards per rolling 24 months.

American Express cards are my second favorite cards behind Chase. With Citibank coming in third. Capital One has been making many improvements over the past few years to come in as my fourth favorite.

Finally US Bank and Barclays tie for my fifth favorite. I’ve also had cards with BBVA Compass, Wells Fargo, Discover & TD Bank in the past.

There are just so many different credit cards you can get and new cards are always being introduced. It’s an endless supply of miles, points, and cash back.

So get through the Chase family of credit cards per the recommendations above in the next few months. And be sure to subscribe The Art of Travel Hacking website and browse recommended card at: https://dkr.lmu.mybluehost.me/credit-cards/

Don’t Forget to Support this FREE Course

Hopefully you have been finding this FREE course helpful (and there is a bunch more lessons to come). If you have, I would be grateful of your support by applying for at least one of your first credit cards using one of my affiliate links above. This will keep this course FREE and send me on some more trips 🙂

Need to Knows

- It’s a good practice to take a screenshot of the credit card you are applying for in case of issue with bonus

- Get familiar with the fine print and offer details – you can typically answer all of your own questions about an offer

- Don’t forget to use a spreadsheet to track details about the credit card (date opened, closed, annual fee, etc)

- Remember to include your award program account number if you already have one on a credit card application to avoid getting duplicate accounts

- Support this FREE course by applying for your first credit card using one of the links above – THANK YOU!

It’s finally time to apply for your first credit card! Are you ready?